CS3D Explained: What the EU's New Supply Chain Due Diligence Rules Mean for SME Suppliers

The Corporate Sustainability Due Diligence Directive is reshaping the way large companies manage their supply chains — and if you're an SME supplier, it directly affects you, even if you're not in scope.

What Is the CS3D — and Why Does It Matter Right Now?

The Corporate Sustainability Due Diligence Directive (CS3D, also known as CSDDD) entered into force on 25 July 2024. This EU legislation requires large companies to identify, prevent, mitigate, and account for negative human rights and environmental impacts — not just within their own operations, but across their entire value chain.

Think of it as a significant shift in how corporate responsibility is enforced: rather than simply disclosing sustainability data, companies in scope are now legally required to take concrete action to address risks wherever they arise in their supply chain, from raw material sourcing all the way through to distribution.

The key word here is entire. That means your large corporate clients — the grand comptes — will be looking closely at their suppliers, their suppliers' suppliers, and beyond. As an SME operating within those chains, the consequences of CS3D reach your business directly, even if the law does not formally apply to you.

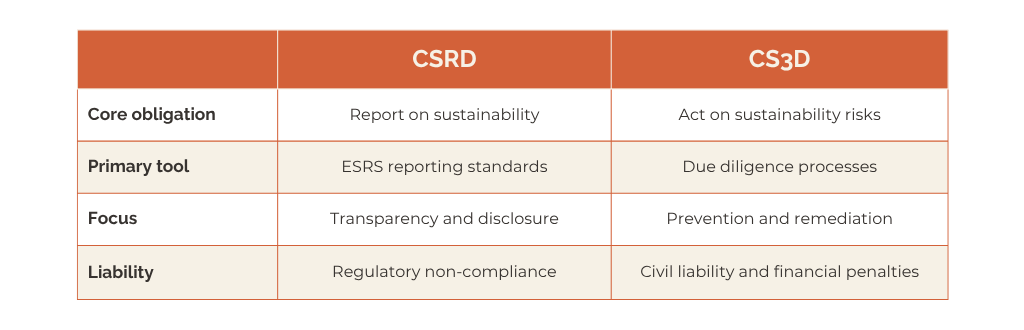

CS3D vs CSRD: Understanding the Difference

Many business owners confuse the CS3D with the Corporate Sustainability Reporting Directive (CSRD). They are related but fundamentally different frameworks, and it is worth understanding what sets them apart.

The CSRD: A Reporting Obligation

The CSRD is focused on transparency. It requires in-scope companies to publish detailed sustainability reports covering environmental, social, and governance (ESG) topics. These reports must follow structured European Sustainability Reporting Standards (ESRS) and be included as part of the company's annual management report. The CSRD answers the question: "What are you doing, and what is your impact?"

The CS3D: An Action Obligation

The CS3D goes further. Rather than simply asking companies to report on their practices, it requires them to actively embed due diligence into their governance, risk management, and supplier relationships. Companies must map their value chains, identify where human rights or environmental risks exist, and take measurable steps to address those risks. The CS3D answers the question: "What are you actually doing about it?"

A Simple Way to Remember the Difference

Both directives are complementary pillars of the EU's broader sustainability framework, and many large companies will need to comply with both.

Updated Deadlines: What Changed Under the Omnibus Package

In February 2025, the European Commission proposed its Omnibus I simplification package, introducing significant changes to both the CSRD and CS3D timelines and thresholds. Following political agreement by the European Parliament in December 2025 and formal adoption by the Council of the EU, the directive entered into force on 18 March 2026 and is now settled law.

Key Changes to the CS3D Timeline

The original CS3D set out a phased implementation schedule. Under the revised Omnibus framework, this has been replaced with a single compliance date: Member States must transpose the amended directive into national law by 26 July 2028, with in-scope companies required to comply from 26 July 2029.

Which Companies Are Directly In Scope?

Under the revised thresholds, the CS3D applies to:

EU companies with more than 5,000 employees and a global net turnover exceeding €1.5 billion

Non-EU companies generating more than €1.5 billion in net turnover within the EU

These thresholds are assessed on a standalone or consolidated group basis.

What This Means in Practice

While the headline deadline is 2029, it would be a mistake for SMEs to treat this as a reason to wait. Large companies are already preparing their compliance frameworks today. Their supplier due diligence processes — and the information requests that come with them — will arrive well before the formal deadline.

How CS3D Affects SMEs: The Trickle-Down Effect

SMEs are not directly bound by the CS3D. However, this does not mean they are unaffected. Quite the opposite.

Large corporations in scope will need to demonstrate that they have conducted due diligence across their value chains. To do so, they will need data, documentation, and assurances from their suppliers — including small and mid-sized businesses like yours.

In concrete terms, this means you can expect:

Sustainability questionnaires from large clients asking about your environmental and social practices

Requests for supporting documentation: policies, certifications, energy consumption data, supplier codes of conduct

Audits or site visits in higher-risk procurement categories

Contractual clauses requiring suppliers to meet minimum ESG standards

Requests to complete the VSME (see below) as a standardised evidence framework

For SMEs that are well-prepared, this is an opportunity to differentiate. For those who are not, it risks becoming a barrier to retaining and winning contracts with large-account clients.

The Role of ESRS and VSME: The Standards You Need to Know

Two sets of standards sit at the heart of the EU’s sustainability reporting framework, and both are relevant to SMEs navigating the CS3D ecosystem.

ESRS: European Sustainability Reporting Standards

The ESRS are the detailed technical standards used by companies subject to the CSRD to structure and publish their sustainability disclosures. They cover topics ranging from climate change and biodiversity to labour rights and supply chain conduct. As of May 2026, a revised and simplified version of the ESRS is in public consultation, with formal adoption expected by September 2026. These revised standards reduce mandatory reporting requirements and now include explicit alignment with CS3D due diligence obligations. They are expected to apply from financial year 2027 onwards.

As a supplier, you may encounter ESRS-derived questions in the information requests you receive from large clients. Understanding the structure of these standards helps you anticipate what data your clients will need from you.

VSME: The Voluntary Standard for SMEs

The VSME — Voluntary Standard for SMEs — is a simplified, proportionate reporting framework developed specifically for companies with fewer than 1,000 employees and an annual turnover below €50 million.

This is particularly significant because the European Commission has recommended that large companies limit their information requests from SME suppliers to the content provided by the VSME. This "value chain cap" introduced under Omnibus I is designed to prevent smaller businesses from being overwhelmed by excessive data demands flowing down from large corporations.

In practical terms, completing a VSME-aligned self-assessment provides you with a ready-made, standardised response to the sustainability questionnaires your clients will send. It demonstrates proactive transparency, reduces back-and-forth, and positions your business as a reliable and forward-thinking supply chain partner.

Why SMEs Should Act Now — Not in 2029

It is tempting to view 2029 as a comfortable horizon. But the businesses that will benefit most from the CS3D shift are those that begin preparing today.

Here is why early action makes strategic sense:

1. Your clients are already building their frameworks. Large companies need to demonstrate multi-year due diligence. They will begin qualifying and categorising their suppliers long before the compliance deadline arrives.

2. Procurement decisions are shifting. ESG criteria are increasingly embedded in supplier selection processes. Companies that cannot provide credible sustainability evidence risk being deprioritised or excluded.

3. The VSME is your competitive tool. Rather than waiting to receive a questionnaire you have never seen before, completing a VSME-aligned assessment now gives you a clear picture of where you stand — and where you need to improve.

4. It is not just about compliance; it is about resilience. Understanding your own environmental and social footprint helps you manage risks, reduce costs, and build a more sustainable business model for the long term.

Summary: What the CS3D Means for Your Business

The CS3D represents a fundamental shift in how environmental and human rights responsibility is distributed across supply chains. Large corporations can no longer treat sustainability as a matter of internal reporting; they are now legally required to put in place robust processes to identify and prevent adverse impacts across their entire value chain.

It is important to understand what this accountability means in practice. A large company will not automatically be held liable for every wrongdoing that occurs somewhere in its supply chain — for instance, the use of child labour by a distant sub-supplier. What the law requires is that the company has implemented adequate due diligence to identify, prevent, and address such risks. If it has failed to do so, it can face consequences at two levels: administrative sanctions (fines of up to 3% of worldwide net turnover, imposed by national supervisory authorities) and civil liability under national law, where victims can seek compensation for damages resulting from a failure of due diligence. Infringement decisions must be made public for at least five years — a significant reputational risk in itself.

As an SME supplier, you sit at the centre of this transformation. The questionnaires, audits, and contractual requirements that come your way are not administrative obstacles — they are the direct expression of a legal duty that your clients are being asked to discharge.

The businesses that prepare now, understand the standards (particularly the VSME), and build credible, documented sustainability practices will be the ones that strengthen their client relationships, win new contracts, and navigate the coming decade of regulatory change with confidence.

Do you want to understand how to complete a VSME self-assessment or prepare for a supplier sustainability audit?

Get in touch — we help SMEs translate complex regulatory requirements into practical, actionable steps.